📊 Performance

- Less than half of individual stocks generated positive lifetime buy-and-hold returns.

- Only 42.6% of stocks outperformed one-month US Treasury bills.

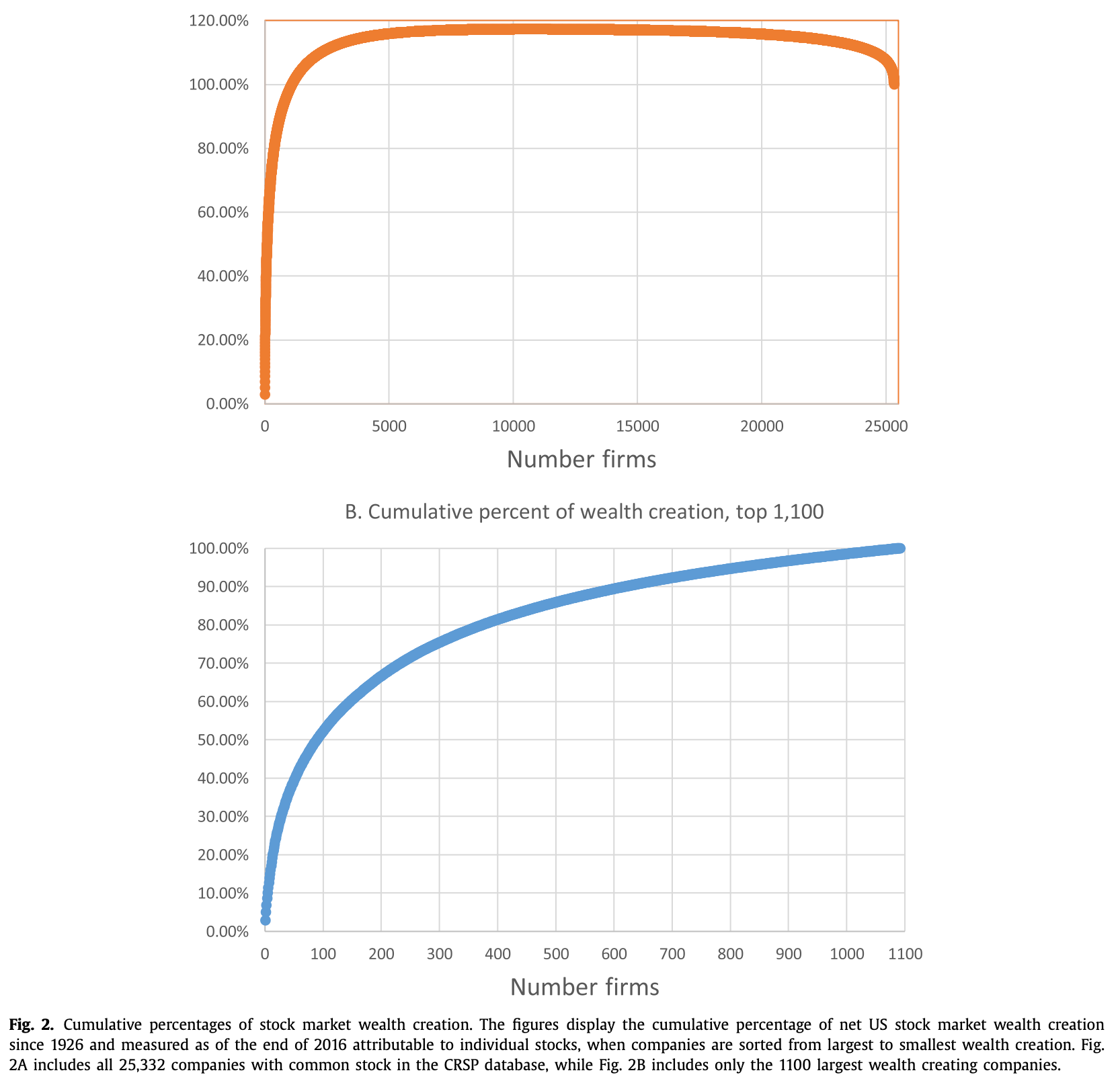

- The top 4% of stocks accounted for all net wealth creation in the US market since 1926.

- The median stock’s return was negative, emphasizing the impact of return skewness.

💡 Key Idea

Stock markets as a whole outperform safe investments, but most individual stocks fail to do so. Market gains are driven by a small fraction of stocks, creating a positively skewed return distribution.

📚 Economic Rationale

The findings challenge the assumption that most stocks provide a risk premium over risk-free assets. Instead, skewness in stock returns plays a major role. The small subset of extreme winners generates overall stock market gains, while the median stock lags behind.

🚀 Practical Applications

- Portfolio Diversification is Key – Concentrated stock portfolios have a high probability of underperformance.

- Passive Investing Works – Market-cap-weighted indices benefit from the outsized gains of a few winning stocks.

- Stock Selection is Difficult – Investors aiming to pick winners must identify the small fraction of stocks that drive market returns.

🛠️ How to Do It

Data

- CRSP monthly stock return data from 1926–2016.

- Market-cap-weighted vs. equal-weighted portfolios.

- Treasury bill returns for comparison.

Model/Methodology

- Buy-and-hold returns analyzed for all individual stocks.

- Wealth creation measured as market value accumulation above Treasury bill rates.

- Skewness and concentration effects explored using bootstrap simulations.

Strategy

- Avoid poorly diversified portfolios – Skewed stock returns mean missing out on top performers is costly.

- Favor systematic investing – Exposure to broad market indices captures the winners without excessive risk.

- Use historical data to inform risk assumptions – Investors should expect most stocks to underperform benchmarks.

📊 Table or Figure

📌 The top 1,092 firms (4% of the market) account for all net stock market wealth creation since 1926, while the bottom 96% of firms collectively matched Treasury bill returns.

📄 Paper Details

- Author: Hendrik Bessembinder

- Journal: Journal of Financial Economics (2018)

- DOI: 10.1016/j.jfineco.2018.06.004